Hello. This is Stanton Jones with a special recap of the most important things you need to know from the 1Q24 ISG Index Call.

If someone forwarded you this briefing, consider subscribing here.

1Q24: Quick Look

Managed services demand slowed slightly in the first quarter due to weakness in the Americas, while cloud demand returned from strength in IaaS. Provider AI revenues are growing but are being limited by flat IT budgets. Watch the full call replay here.

Data Watch

What You Need to Know

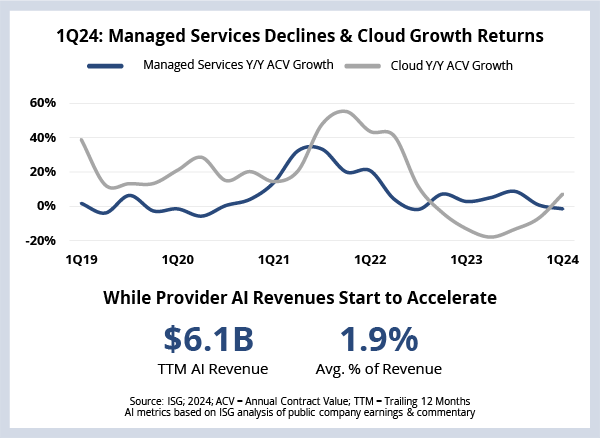

Managed services annual contract value declined 1.4% Y/Y primarily due to weakness in the Banking and Financial Services (BFSI) sector in the U.S., which was down 18% Y/Y. Even still, ACV was robust, totaling more than $10 billion for the third quarter in a row.

Despite the weak results in the Americas, managed services ACV grew in other areas. EMEA was up 3% on strong demand for BPO, and Asia Pacific was up 18% on strong demand in BFSI.

Cloud ACV was up 7% Y/Y. This was the best quarterly result for cloud services since 2022 and was largely based on demand for cloud infrastructure with IaaS ACV up 11% Y/Y. Telecom and Media, Travel and Transportation and Energy were the fastest-growing industries in IaaS in Q1.

Meanwhile, Software-as-a-Service ACV fell in 1Q24. ACV was down 2% Y/Y primarily due to weakness in areas like customer relationship management, IT service management and ERP. These three make up almost 50% of the ACV in our SaaS coverage, so when they are down, the entire segment tends to be down.

Providers are starting to generate notable revenue from AI. We’re estimating over $6 billion of trailing-12-month revenue from AI projects in the firms we cover. It will take time for this revenue to move into the “run” portion of providers’ businesses, but it is significant in that, on average, it amounts to nearly 2% of total revenues.

As we’ve discussed at length over the past couple of months, enterprises have big plans around AI, including doubling the number of AI-enabled applications in their portfolio and doubling their AI spending in the coming year. It’s important to note that IT budgets are largely flat, so at least for today, if AI funding is coming from IT, it’s coming at the expense of another area.

What’s Next

The weakness in the Americas BFSI sector is concerning. It represents 25% of the ACV in the Americas and more than 30% of the total ACV in the sector. With the higher-than-expected inflation news in the U.S. this week, rate decreases may be delayed, which is likely to negatively impact technology spending in the BFSI sector. Additionally, manufacturing in EMEA continues to be under pressure, and smaller discretionary awards were down in Q1 as well.

Growth in the number and value of managed services deals in 2024 is predicated on these three areas returning to normal. And, while we anticipate technology spending in BFSI to improve in the second half of the year (especially in areas like lending, payments and cards), continuing inflation may delay that. This is the primary reason we’re lowering our managed services forecast to 3% for the full year.

We’re maintaining our cloud forecast at 15% based on the strength we’re seeing in IaaS. It does appear that much of the optimization work that happened over the past 18 months is coming to a close, and now enterprises are looking for AI-related software and services. This demand stands to benefit both IaaS and SaaS providers and is reflected in our forecast.

You can watch the quarterly ISG Index call here.

About the author

Stanton Jones

Stanton helps enterprise technology leaders, IT service providers and buy- and sell-side professionals make sense of the global IT services sector. Stanton's weekly briefing - the Index Insider - is read by thousands of industry stakeholders each week.